What is a GST Return Filing?

Filing of return under the GST Act is specified under section 37-48 of CGST Act & provisions relating to the form & manner of filing is dealt in rule 59-84 of CGST Rules.

A GST return is a document containing details of:

Eligibility & Persons require to file LUT in Form GST RFD-11?

A LUT is required to be filed online by an exporter who intends to make exports without the payment of IGST irrespective of Export of Goods or Services.

- Outward supplies (Sales) & the taxes collected on the same

- Inward supplies (Purchase) & the tax paid for the same

- Payment of output GST on self-assessment basis

- Claiming of Input Tax Credit (ITC)

- the above details are to be furnished by a registered person on monthly/quarterly, annual or final return basis (as the case may be).

- All the returns in GST are to be filed electronically.

Who Should File GST Return?

Persons Required to File GST Return:

- Every Normal Taxpayer Registered under GST,

- Taxpayer opted for Composition Levy

- Non-Resident Taxable Person (NRTP)

- Overseas Supplier of OIDAR Services

- Input Service Distributor (ISD)

- Tax Deductor (u/sec 51)

- E-Commerce Tax Collector (u/sec 52)

- Taxpayer whose registration has been cancelled / surrendered

- Casual Taxable Person

- Persons having a Unique Identity number (UIN)

Benefits or Purpose of GST Return Filing

- Compliance verification program of tax administration

- Finalization of tax liabilities of the taxpayer within a stipulated period of Limitation

- Computation and Claiming of Input Tax Credit as per Section 16

- Providing necessary inputs for taking policy decisions

How to file GST Return Online (Step by Step Process)

Types of GST Return

| Return | Who Files | Description |

|---|---|---|

| GSTR1 | Normal TP including Casual TP | Monthly Statement of Outward Supplies |

| GSTR 3B | Normal TP including Casual TP | Simplified Monthly Return |

| GSTR 4 | Composition TP | Annual Return |

| GSTR 5 | Non-Resident TP | Monthly Return for NRTP |

| GSTR 5A | OIDAR Service Provider | Monthly Return |

| GSTR 6 | Input Service Distributor | Monthly Return, Details of ITC received & distribution of ITC |

| GSTR 7 | Tax Deductor (u/sec 51) | Monthly Return, Details of Tax Deducted |

| GSTR 8 | ECO- tax Collector (u/sec 52) | Monthly Statement for E-Commerce Operator depicting supplies effecting through it |

| GSTR 9 | Normal TP excluding Casual TP | Annual Return |

| GSTR 9A | TP opted for Composition Levy | Annual Return |

| GSTR 9B | ECO- tax Collector (u/sec 52) | Annual Statement |

| GSTR 9C | Normal TP excluding Casual TP, whose aggregate TO exceeds 5 crores during a FY | Self-certified reconciliation statement |

| GSTR 10 | TP Whose Registration has been Cancelled / surrendered | Final Return |

| GSTR 11 | UIN Holders | During those months when they make inward supplies |

Due Dates for GST Return

| Return | Due Date | Who Files |

|---|---|---|

| GSTR 1 | 11th of the next month (refer note 1) | Normal TP including Casual TP |

| GSTR 3B | 20th of the next month (refer note 2) | Normal TP including Casual TP |

| GSTR 4 | 30th April of Following FY | Composition TP |

| GSTR 5 | 20th of the month succeeding the tax period or within 7 days after expiry of registration whichever is earlier | Non-Resident TP |

| GSTR 5A | 20th of the next month | OIDAR Service Provider |

| GSTR 6 | 13th of the next month | Input Service Distributor |

| GSTR 7 | 10th of the next month | Tax Deductor (u/sec 51) |

| GSTR 8 | 10th of the next month | ECO- tax Collector (u/sec 52) |

| GSTR 9 | 31st December of the next Financial Year | Normal TP excluding Casual TP |

| GSTR 9A | 31st December of the next Financial Year | TP opted for Composition Levy |

| GSTR 9B | 31st December of the next Financial Year | ECO- tax Collector (u/sec 52) |

| GSTR 9C | 31st December of the next Financial Year | Normal TP excluding Casual TP, whose aggregate TO exceeds 5 crores during a FY |

| GSTR 10 | Within 3 months of Later of:a) The Date of cancellation order orb) Date of cancellation | TP Whose Registration has been Cancelled / Surrendered |

| GSTR 11 | 28th of Following Month | UIN Holders |

Note 1: The due dates for GSTR-1 are based on your turnover. Entities with aggregate annual turnover up to Rs.5 crore have an option to file quarterly returns under the QRMP scheme and filing of GSTR 1 is due by the 13th of the month following the relevant quarter.

Whereas, those taxpayers who do not opt for the QRMP scheme or have a total turnover above Rs.5 crore requires to file the return every month on or before the 11th of the next month.

Note 2:

Annual Turnover Up to INR 5 Cr in Previous FY and opted for Quarterly Filing

GST Return Filing Due date is 22nd of the next month For State 1 Group (Chhattisgarh, Madhya Pradesh, Gujarat, Karnataka, Maharashtra, Kerala, Goa, Tamil Nadu, Telangana, Andhra Pradesh, Daman & Diu, and Dadra & Nagar Haveli, Lakshadweep, Puducherry, Andaman and Nicobar Islands)

GST Return Filing Due date is 24th of the next month For State 2 Group (Himachal Pradesh, Punjab, Uttarakhand, Haryana, Bihar, Rajasthan, Uttar Pradesh, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, Jharkhand, West Bengal, Odisha, Jammu and Kashmir, Ladakh, Chandigarh, Delhi)

How to file GST Return Online (Step by Step Process)

GST Return Filing Process – General steps applicable for filing all types of GST Returns

Step 1: To File GST Return Online , Visit the GST portal – https://www.gst.gov.in

Step 2: Log in to the GST Portal by entering a valid username & password.

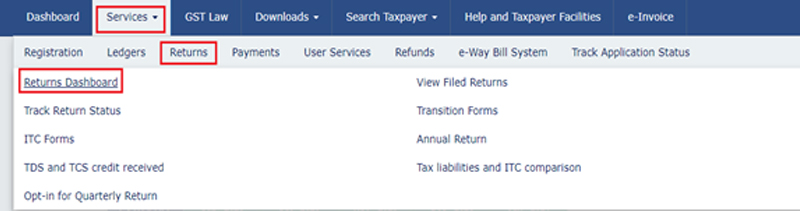

Step 3: Step 3: Navigate to ‘Services’ > ‘Returns’ > ‘Returns Dashboard’.

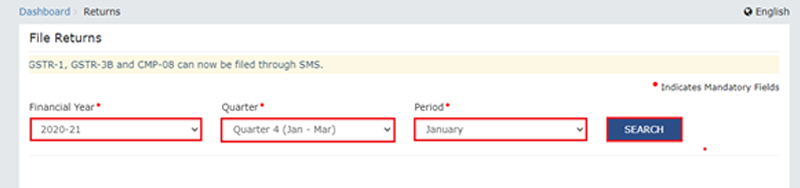

Step 4: This displays the ‘File Returns’ page. Select the ‘Financial Year’ & ‘Return Filing Period’ as applicable from the drop-down list, then click the ‘SEARCH’ button.

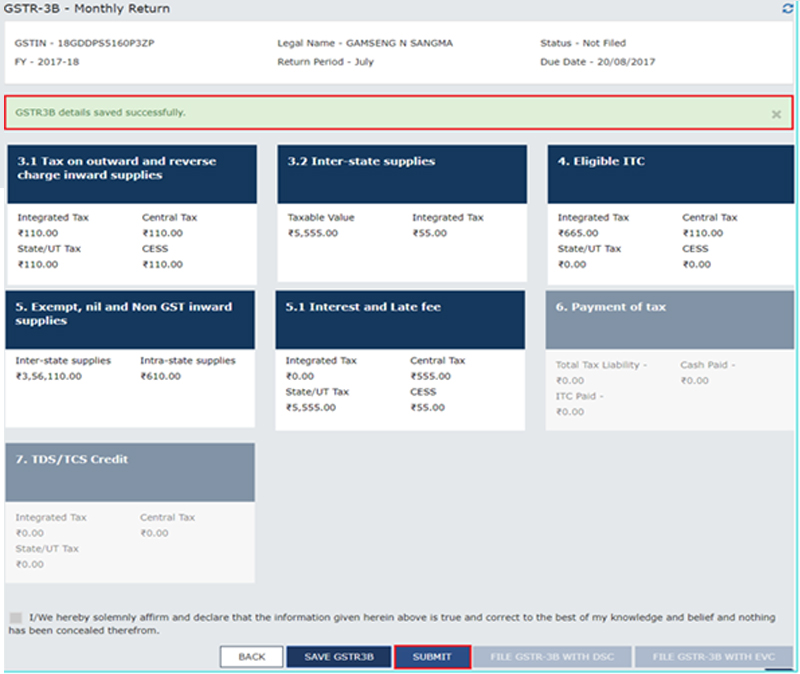

Step 5: After selecting the Return and period for which return is to be filed, enter values in each tile displayed as may be applicable.

Step 6: :Click the ‘SAVE’ button at the bottom of the page after all details are added. A message is displayed on the top of the page confirming that data is successfully saved.

Step 7: Once all the details are saved, the ‘SUBMIT’ button at the bottom of the page is enabled. Click the ‘SUBMIT’ button to submit the finalized GST return.

Step 8: Now, you can view the draft GST return by clicking on ‘PREVIEW DRAFT GST Return’. You will also see that the ‘Payment of Tax’ tile is enabled (if applicable) after the successful submission of the return. Click the ‘Payment of Tax’ tile, and pay the tax.

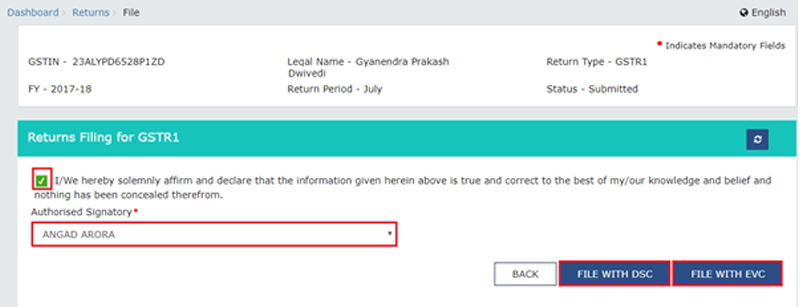

Step 9: Select the checkbox for declaration. From the ‘Authorised Signatory’ drop-down list, choose the authorized signatory. Click the ‘FILE GSTR-3B WITH EVC’ or ‘FILE GSTR-3B WITH DSC’ button.

Step 10: GST Return Filing Status – A success message will be displayed on the screen along with an ARN (Acknowledgment Reference Number)

Late Fee/Interest for Non-Filing of GST Return

As per the GST Acts, for intrastate supplies, the late fee should be paid for GSTR1 & GSTR 3B under both the CGST and SGST Act as follows:

| Name of Act | Late Fee For every day of delay |

|---|---|

| CGST Act | Rs. 25 |

| SGST Act | Rs. 25 |

| Total Late Fee to be paid per day | Rs. 50 |

Late fee for GST Nil return filing mentioned below:

| Name of Act | Late Fee For every day of delay |

|---|---|

| CGST Act | Rs. 10 |

| SGST Act | Rs. 10 |

| Total Late Fee to be paid per day | Rs. 20 |

Late fee For GST annual returns (GSTR-9):

| Name of Act | Late Fee For every day of delay |

|---|---|

| CGST Act | Rs. 100 |

| SGST Act | Rs. 100 |

| Total Late Fee to be paid per day | Rs. 200 |

The CGST Act has fixed a maximum late fee of an amount calculated at 0.25% of the Turnover for the financial year.

As per the 43rd GST Council Meeting, the maximum late fee is reduced to the following amount:

- In the case of nil GSTR-1 and GSTR-3B filing, the maximum late fee charged shall be capped at Rs.500 per return (i.e., Rs. 250 each for CGST & SGST).

- In GSTR-1 and GSTR-3B other than nil filing, the maximum late fee is fixed based on the annual turnover slab, as follows:

- In case the annual aggregate turnover in the previous financial year is up to Rs.1.5 crore then the late fee of maximum Rs. 2,000 per return can only be charged (i.e., Rs.1000 each for CGST and SGST).

- In case the annual aggregate turnover is between Rs.1.5 crore and Rs.5 crore then the maximum late fee of Rs.5,000 per return can only be charged (i.e., Rs. 2500 each for CGST and SGST).

- In case the annual aggregate turnover exceeds Rs.5 crore then a late fee of a maximum of Rs.10,000 (i.e., Rs. 5000 each for CGST and SGST) can be charged.

- Interest on delayed filing of GST Return

- Interest to be paid @18% per annum. It has to be calculated by the taxpayer on Net tax Liability. The interest is to be calculated from the next day of filing to the date of payment.

Glossary

| Terms Used | Full-Form |

|---|---|

| IGST | Integrated GST |

| CGST | Central GST |

| SGST | State GST |

| TP | Taxpayer |

| NRTP | Non-Resident Tax Payer |

| ITC | Input Tax Credit |

| OIDAR | Online Information Database Access and Retrieval services |

| UIN | Unique Identity Number |

| TO | Turnover |

| FY | Financial Year |

Choosing eAuditor Office

eAuditor is a leading business service platform in India that offers end-to-end GST services. We make GST return filing very seamless and simple.

When GST return filing is outsourced to eAuditor a dedicated GST consultant is assigned to the business.

This dedicated consultant would reach out to you every month and collect the necessary information, prepare the GST returns and help in filing the GST returns.

There will be absolutely no delay from our end in the process. You will get GST return filed before the due date by availing of our services.